The variable overhead efficiency variance can be confusing as it may reflect efficiencies or inefficiencies experienced with the base used to apply overhead. For Blue Rail, remember that the total number of hours was “high” because of inexperienced labor. These welders may have used more welding rods and had sloppier welds requiring more grinding.

In a similar vein the standard quantity is the budgeted cost driver consumption per unit produced.

In the standard costing system, the labor costs are posted at the standard cost of 3,750 represented by the debit to the work in process inventory account.

That means accumulating some costs at the job-level and some costs at the process-level (hybrid systems are sometimes called “operation costing”).

Notice that this differs from the budgeted fixed overhead by $10,800, representing an unfavorable Fixed Overhead Volume Variance.

Note that unfavorable variances (negative) offset favorable (positive) variances.

Favorable overhead variances are also known as “overapplied overhead” since more cost is applied to production than was actually incurred.

( Reasons of variances:

(See MAAW’s illustration of the T-accounts the journal entries go to. “Factory Overhead” in this illustration is the same as the Overhead Control account). With a little investigation the firm could use this variance to develop a plan to improve profits next period. But total budget variance, the only variance I’ve introduced thus far, could be caused by hundreds, thousands, even millions of things. Managers are hardly any closer to knowing how to improve profits simply by knowing total budget variance.

Variable Overhead Variance Journal Entry

To operate a standard costing system and allocate variable overhead, the business must first decide on the basis of allocation. Various methods can be used to allocate the variable overhead including for example, the number of direct labor hours used in production or the number of machine hours used. Additionally the method of allocation is more fully discussed in our applied overhead tutorial. When undertaking standard costing variance analysis, it is important to understand that the costs and therefore the variances are all interrelated.

2.4 Quick Note on Multi-product Firms’ Sales Volume Variance

The production that is acceptable (not rejected products) and which is assigned manufacturing costs of direct materials, direct labor, and manufacturing overhead. The Direct Materials Inventory account is reduced by the standard cost of the denim that was removed from the direct materials inventory. Let’s assume that the actual quantity of denim removed from the direct materials inventory and used to make the aprons in January was 290 yards.

Clearing the Variable Overhead Variance Accounts

In the standard costing system, the variable overhead is posted at the standard cost of 1,250 represented by the debit to the work in process inventory account. In this example, the variable overhead rate variance is positive (50 favorable), and the variable overhead efficiency variance is also positive (100 favorable), resulting in an overall positive variable overhead variance (150 favorable). Manufacturing overhead costs refer to the costs within a manufacturing facility other than direct materials and direct labor. Manufacturing overhead includes items such as indirect labor, indirect materials, utilities, quality control, material handling, and depreciation on the manufacturing equipment and facilities, and more.

Hence, the balance in the inventory account is constantly or perpetually changing. Under this system there is a general ledger account Cost of Goods Sold. Note that the entry shown previously uses standard costs, which means cost of goods sold is stated at standard cost until the next entry is made.

The variance is calculated using the variable overhead efficiency variance formula. This formula takes the difference between the standard quantity and the actual quantity of variable your 2021 guide to creating a culture of accountability in the workplace overhead allocated, and multiplies this by the standard variable overhead rate. A good manager will want to explore the nature of variances relating to variable overhead.

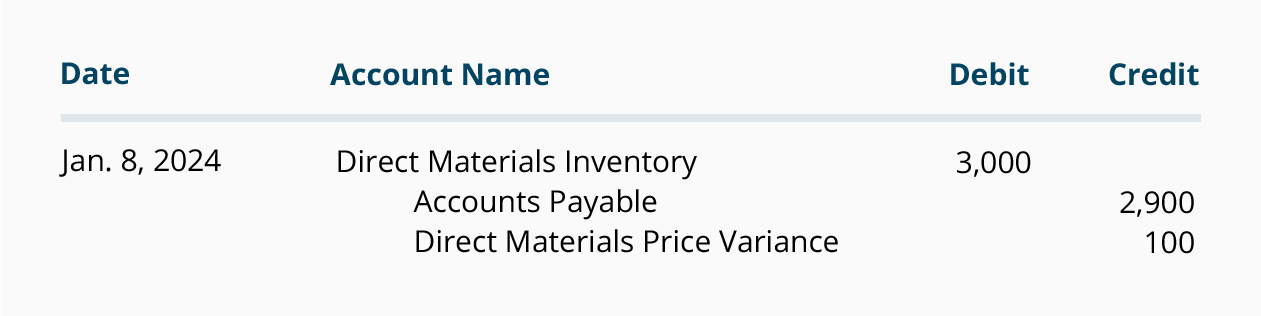

Notice that the raw materials inventory account contains the actual quantity of direct materials purchased at the standard price. Accounts payable reflects the actual cost, and the materials price variance account shows the unfavorable variance. Unfavorable variances are recorded as debits and favorable variances are recorded as credits. Variance accounts are temporary accounts that are closed out at the end of the financial reporting period. We show the process of closing out variance accounts at the end of this appendix. Notice that the raw materialsinventory account contains the actual quantity of direct materialspurchased at the standard price.

Or, one can perform the algebraic calculations for the price and quantity variances. Note that unfavorable variances (negative) offset favorable (positive) variances. A total variance could be zero, resulting from favorable pricing that was wiped out by waste. A good manager would want to take corrective action, but would be unaware of the problem based on an overall budget versus actual comparison. A variance is the difference between an actual measured result and a basis, such as a budgeted amount. In many accounting applications, a variance is considered to be the difference between an actual cost and a standard cost.